Last updated: 10 Dec 2025

Planning for Small Sites

Permission impossible for small sites and SME home builders

Contents

Foreword

Neil Jefferson, Chief Executive

Home Builders Federation

Small- and medium-sized (SME) home builders continue to face a challenging landscape when it comes to delivering homes on smaller sites. Five years on from Lichfields’ previous research into the journey of small sites, this report makes clear that many of the same barriers remain - and in some cases, they have become even more acute.

The planning process continues to be the most significant challenge for SME home builders. Alongside the lengthy timescales required to secure implementable permission, the increasing complexity, risk, and cost of navigating the system are significant obstacles. These delays and burdens are not only slowing down delivery but are also discouraging SME builders from taking on much-needed smaller developments altogether.

This report shows just how significant these challenges are. On average, it takes around 30 weeks from submission to committee decision, while some small sites have faced even more extreme delays, with a handful taking over three years to achieve permission. Combined with increasing planning fees and obligations, it is clear that the process is too lengthy and too costly.

To address these barriers, this report sets out some practical recommendations to help SMEs bring forward more small sites. Supporting these smaller builders is not just about increasing housing supply and boosting economic growth - these businesses also forge close links with their local communities, ensure a diverse and competitive housing market, and make good use of underutilised land.

I hope the findings of this report will encourage government to take further action to support this vital part of the industry, ensuring that smaller sites and the developers that build them can play their part in tackling the housing crisis.

Oliver Thompson, Chief Executive

Quantum Development Finance

SME home builders are vital to the health of the UK housing market, delivering high-quality, locally sympathetic homes, unlocking underutilised land, and fuelling local economies through skilled jobs and community investment. Yet for many of the businesses we work with, the journey from acquiring a small site to delivering new homes has never been more difficult or uncertain. Their ability to operate successfully is being tested at precisely the time when their contribution is most needed.

As a lender that specialises in supporting SME developers, we see first-hand the challenges these businesses face. From planning delays to rising costs, the barriers to entry and delivery have grown significantly. This report illustrates some of these issues, particularly when navigating the planning system.

Today, 94% of applications miss the statutory determination deadline, and it takes nearly a year on average to secure planning permission, with some schemes taking two to three times longer. And that’s before accounting for the average 515-day negotiation period for Section 106 agreements. For SMEs, these delays have serious implications for cashflow, project viability, and the capacity to reinvest in future developments.

The financial burden is also mounting. Planning fees and obligations continue to rise year on year, while new taxes, levies, and environmental compliance costs are set to place even greater strain on smaller developers. These pressures are becoming increasingly disproportionate, with the system now demanding a level of financial resilience that many SMEs simply cannot continue to absorb.

There are, however, reasons for optimism. Planning reform and support for housebuilders are now firmly on the Government’s agenda, with recent consultations and policy proposals recognising the need to reform the system and accelerate delivery. We hope the data and insights presented here help inform policy discussions and give Government a clearer understanding of the specific challenges faced by smaller housebuilders. If we are serious about fixing the housing crisis, we cannot afford to overlook the vital role of SMEs.

Context

Small sites play a crucial role in housing supply by utilising underused land where larger-scale developments may not be feasible. These sites, defined for this report as developments of up to 150 homes and smaller than 0.25 hectares1, can also typically move from commencement to completion and ultimately sale, much more quickly than larger sites.

As a result, small- and medium-sized (SME) home builders are often able to deliver multiple smaller schemes within a year, contributing significantly to housing supply at a local level.

In addition to their vital contribution to housing supply and economic growth, small sites support local and SME developers, which encourages competition in the market and variety and innovation in the types of homes being built.

However, the efforts of smaller developers are constantly hampered by increasing costs, delays and risks, which discourage future investment from such builders. The Competition and Markets Authority (CMA) Market Study, published in 2024, highlighted the planning system as one of the predominant barriers to entry and expansion of SME home builders, stating that the planning system favours large sites due to lower costs and greater expediency. The high upfront costs and unpredictable delays resulting from the planning process are particularly problematic for SMEs, which lack the financial resilience or capacity to absorb risk of larger developers.

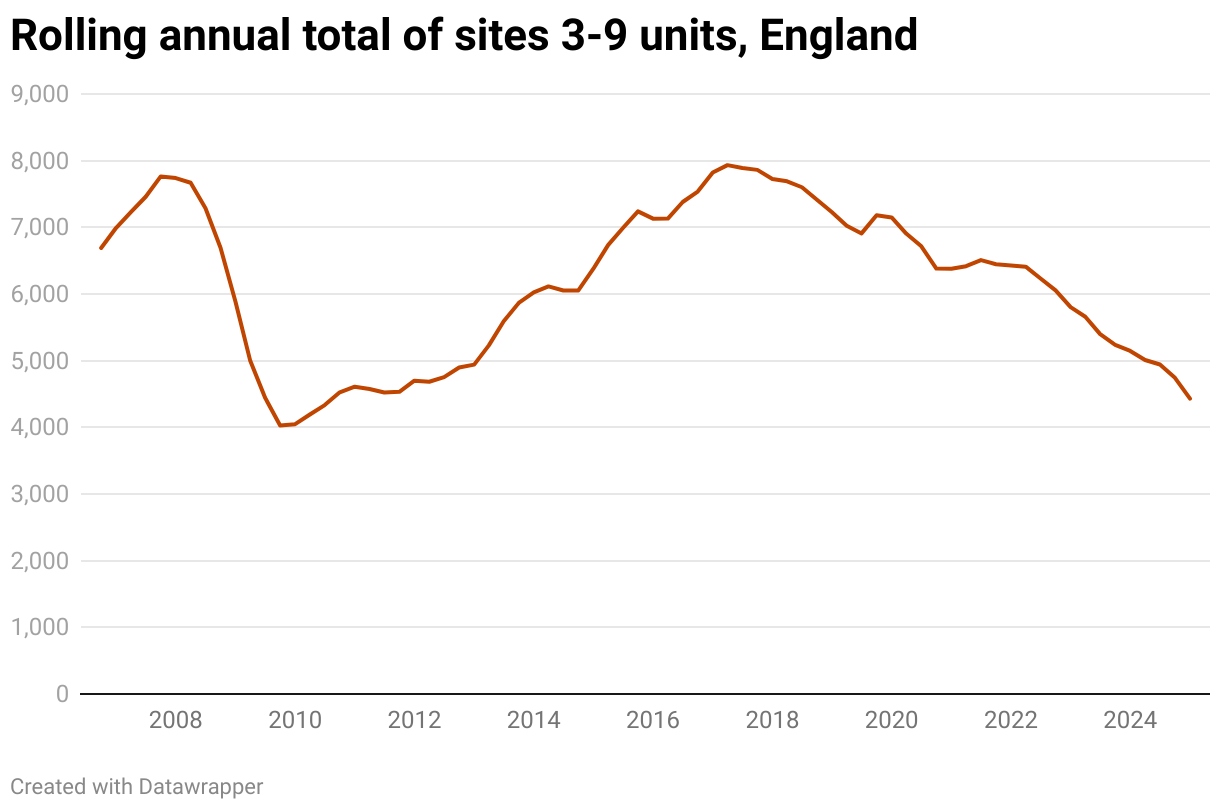

As a result, there has been a long-term reduction in the number of small sites being permissioned, and SMEs are unable to deliver homes at the scale they once could. This can be seen in HBF’s Housing Pipeline Report. The number of sites of 3-9 units2 being granted planning permission in a 12-month period has dropped to the levels seen following the Global Financial Crisis. Although many SME home builders deliver schemes larger than 9 units, this downward trend is now evident across sites of all sizes.

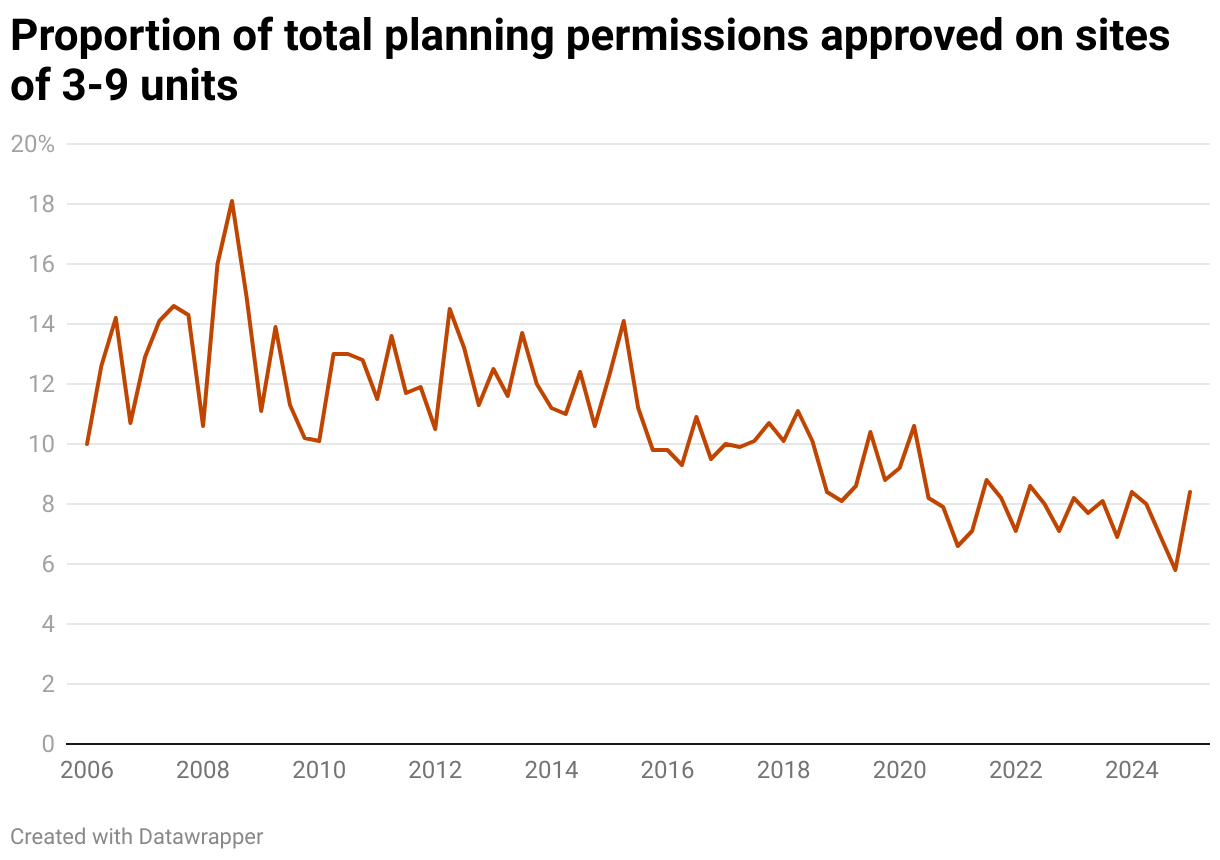

The proportion of total units being delivered on these smaller sites has decreased significantly, too. In 2024, just over 17,000 homes were approved on sites of 3-9 units.3 This compares to around 35,000 units approved in an average 12-month period when the Housing Pipeline Report began recording. To account for market factors, we have also analysed the proportion of newly-permissioned homes coming from these smaller sites. At the peak, in 2008, almost 20% of plots granted planning permissions were on sites of 3-9 units. This has dropped significantly since, now sitting between 6% and 8%.

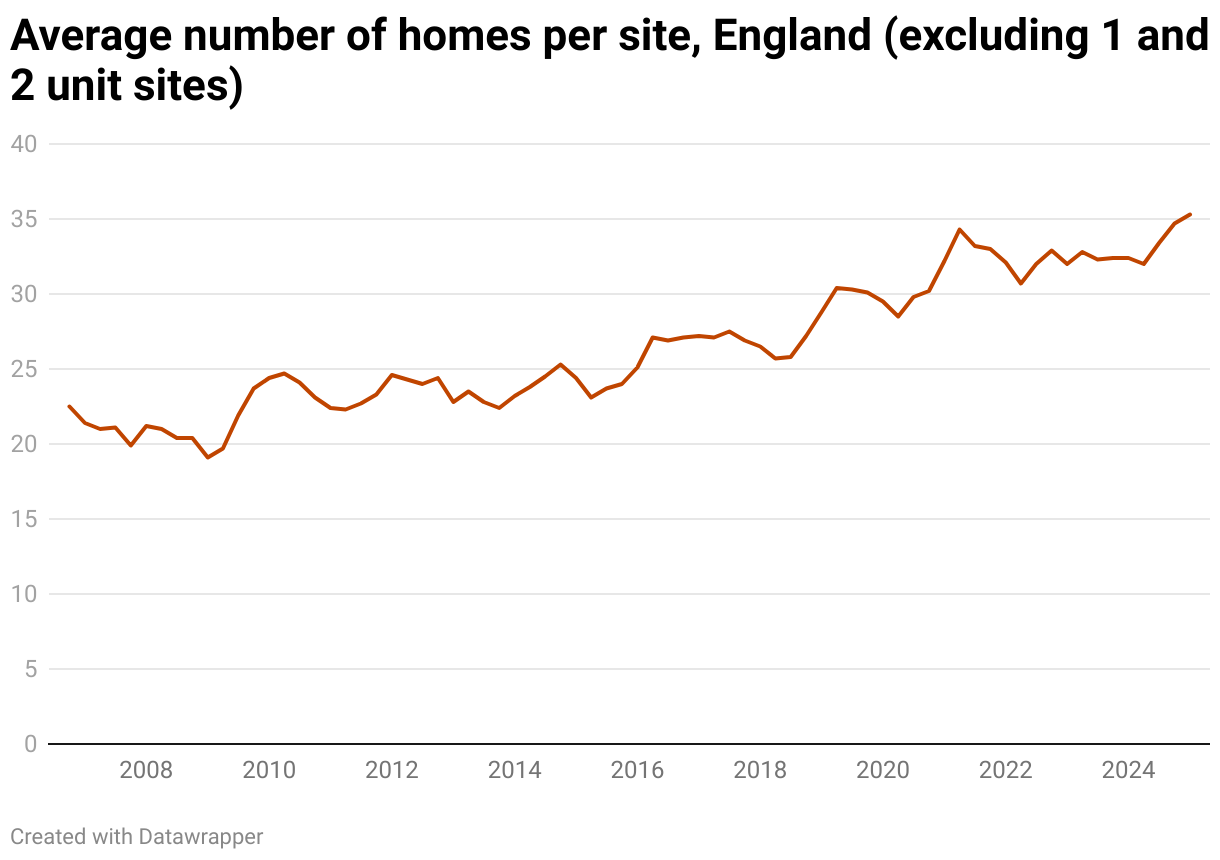

The average site size has increased significantly, too. While during the years 2006-2014, the average number of units per site hovered between 18 and 23, the last decade has seen this number increase significantly, reaching a peak at the end of 2024, by which time the average site size almost doubled compared with a decade previously, to just over 41 units per site.

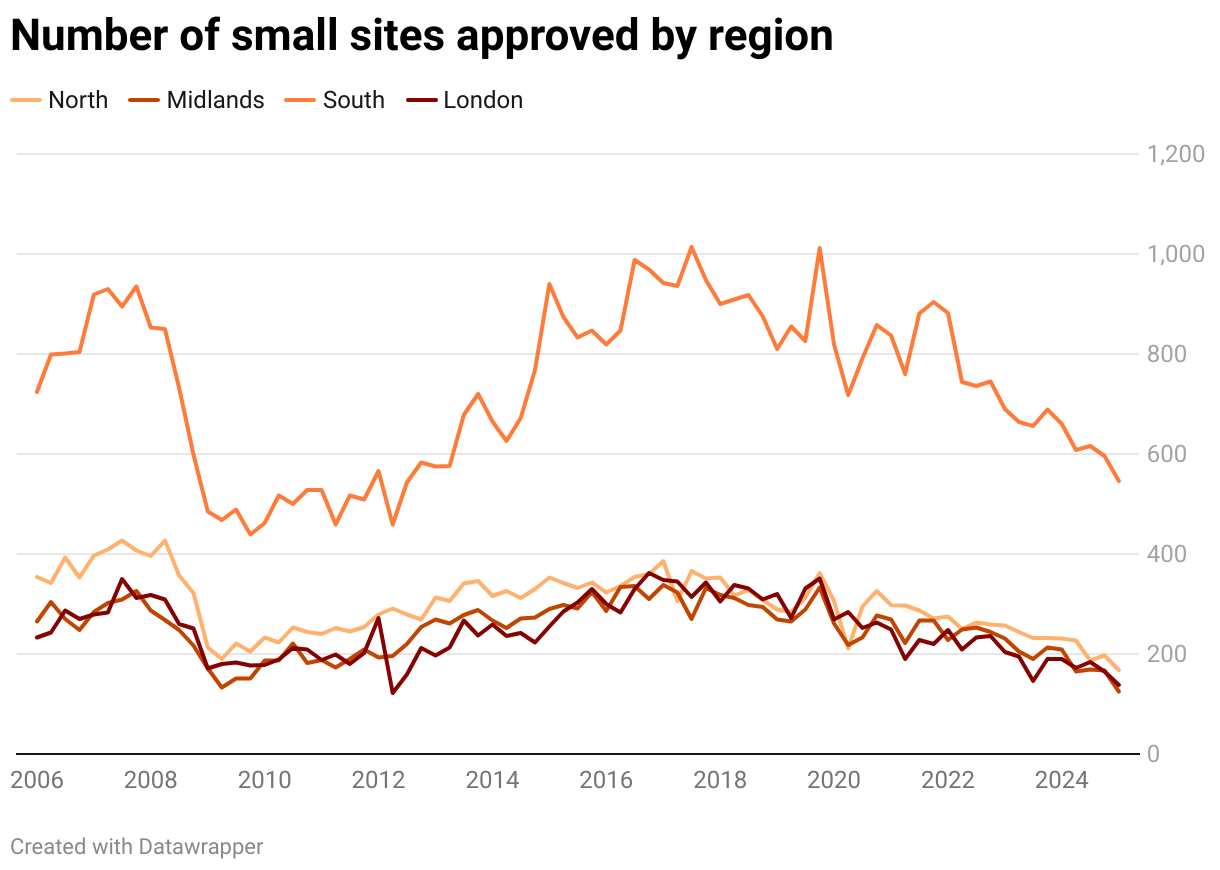

This trend for small sites can be seen across the whole country, with all regions seeing a significant decrease in the number of sites of 3-9 dwellings being granted approval. Even in areas where housing demand is high and land availability should support smaller developments, the overall trajectory remains downward.

As this research explores, the process for getting planning permission on a small site is becoming increasingly difficult for SME developers in terms of both time and cost. In part, this is due to:

- Under-resourced and understaffed Local Planning Authorities (LPAs) - Recent FOI research carried out by HBF showed that 80% of councils are operating at below full staffing capacity in their planning departments.

- Time taken to finalise Section 106 agreements - A lack of standardisation in the drafting of Section 106 agreements often leads to protracted negotiations and inconsistencies across councils, with 76% of local authorities reporting average negotiation timescales exceeding 12 months.

- Delays in responses from statutory consultees - HBF research has found that for Section 38 agreements, which relate to the construction of new highways, the time taken from technical submission to technical approval ranged from two weeks to 103 weeks, and to formal adoption ranged from four weeks to 286 weeks4.

The patterns outlined in the graphs above reflect a planning and policy system that increasingly places growing burdens on SME builders and favours large-scale development.

In the broader policy environment, there are a number of ongoing challenges that are exacerbating the situation further still.

Biodiversity Net Gain (BNG)

BNG requirements have introduced a new set of obligations for developers, mandating measurable environmental improvements. While the principle of BNG is widely supported, its application often disadvantages SME builders and smaller sites. HBF’s analysis of the BNG requirements one year after they were introduced found that:

- 98% of SME builders are finding implementation of the new requirements a challenge, with delays in the process as a result of a lack of local authority capacity being the biggest barrier.

- 94% of respondents said they have experienced delays in processing planning applications due to BNG.

- 90% experienced delays specifically due to insufficient BNG expertise or resources within local authorities.

Building Safety Levy

The forthcoming Building Safety Levy is another concern. Although the levy was initially framed in the context of high-rise developments, it will be payable by developers on all new homes.

From autumn 2026, it is expected that the Building Safety Levy will add thousands of pounds to the cost of building each new dwelling.

For SME home builders already working with tight margins, and amid growing pressure on viability, the risk of another cost could be enough to prevent projects from progressing altogether, which is particularly concerning for those businesses that have never developed higher-rise or mid-rise buildings.

Landfill Tax

In April 2025, the Government launched a new consultation on the Landfill Tax regime, aiming to drive more waste away from landfill. As part of this, it is proposing a shift to a single rate of Landfill Tax.

If implemented, the changes could represent a dramatic increase in costs for many home builders. Indeed, early estimates from HBF suggest that the proposal would amount to a 3,000% rise in Landfill Tax. Effectively, this would amount to a new levy on new homes, potentially adding several thousand pounds in costs per home, and in some cases, more than £10,000.

The impact is expected to be particularly severe for SME home builders. While larger developers may be able to mitigate costs by transporting reusable materials such as topsoil between multiple sites, SMEs, who often operate on just one site, do not have that flexibility. Beyond the direct financial burden, we are concerned that such a significant tax rise could further undermine the viability of the SME home building industry.

Section 106 Affordable Housing

The diminishing interest of Registered Providers (RPs) in acquiring Section 106 Affordable Homes is continuing to impact, delay and stall the delivery of new homes.

Earlier this year, HBF conducted a Freedom of Information (FOI) request with Local Authorities to determine the potential scale of the issue. Analysis of responses from more than 85 Local Authorities, extrapolated to all 317 Local Authorities in England and Wales, indicates around 8,500 S106 units, either under construction or due to commence within 12 months, are not currently under contract with an RP.

This issue is particularly challenging for SME developers as many of these builders depend on project-based financing to support cash flow and initiate construction, but they cannot access these funds without a contract in place to sell the Section 106 homes to RPs or councils.

Furthermore, because SME developers typically work on smaller-scale developments, they often have only a limited number of Affordable Homes to offer to an RP. However, such small, dispersed clusters are generally unattractive to RPs, as managing them across multiple locations is often inefficient, costly and impractical.

While the Government’s announcement at the Spending Review of a new Affordable Homes programme, rent convergence, 10-year rent settlement and access to building safety funding may support RPs in rebuilding their financial capacity over the longer term, immediate action is needed to stop small sites grinding to a halt and SME developers being forced out of business.

Nutrient neutrality

Nutrient neutrality requirements continue to act as a major blocker to housing delivery in dozens of affected local authority areas.

While the impact on larger developers has been partially mitigated through access to strategic mitigation schemes or land for offsetting, this is an admin-heavy and expensive resolution to the issue, making it somewhat inaccessible for those building on smaller sites. As a result, many otherwise deliverable small sites remain stuck in planning limbo, with no clear path forward.

Further increases to planning fees

The Government’s Planning and Infrastructure Bill, once enacted, will enable the sub-delegation of planning fees, allowing Local Planning Authorities (LPAs) to recover the full cost of processing applications through fee revenue. Currently, the annual funding shortfall for LPAs is estimated at £362 million.

However, the potential impact of these fee increases on SME developers could be significant. In fact, MHCLG’s own Impact Assessment for the Bill acknowledges that:

“These increases will likely have an impact on small, micro, and medium-sized businesses who submit planning applications… As these businesses are more likely to submit minor applications (which are estimated to have the greatest funding shortfalls of between 50% and 150%), if LPAs set fees at the level of full cost recovery, it is likely that the fees for minor applications will proportionately increase by a greater rate than fees for major applications, which may not increase by very much, if at all. This could potentially have a disproportionate impact on small, micro, and medium-sized businesses.5”

About this research

This report builds on a 2020 study by Lichfields in partnership with Pocket Living, examining why small sites were not making a more significant contribution to housing delivery in the UK6. The research was prompted by decades of decline in the number of small- and medium-sized (SME) businesses in the home building sector, driven by a range of economic, political, and regulatory challenges.

Based on a sample of 60 developments across London, ranging between 10 and 150 new homes, the 2020 report explored the journey of developments on small sites through the planning process and the constraints and challenges that they encounter.

Five years on, SME developers continue to face significant challenges navigating the delays, costs, and uncertainty of the planning process. To assess progress, the original London sites have now been reviewed to determine whether they have been completed, are under construction, have been sold, or are stalled or cancelled. For completed sites, the research also examines how long they took to deliver.

This research also includes an expanded, in-depth analysis of the planning journeys of small sites in additional urban areas – Birmingham, Liverpool, Manchester, Leeds, and Newcastle upon Tyne.

Specifically, it explores:

- Average timescales from submission to permission

- The impact of delegated decisions on timescales

- The cost of achieving planning permission

Finally, since SME developers building out smaller sites are often the most acutely affected by delays in the planning process, research has also been conducted to assess the impact of the December 2023 increase in planning fees on Local Planning Authorities’ (LPAs) resources and their capacity to determine applications in a timely manner.

Summary of key findings

The remainder of this report sets out the detailed findings of our research and presents our recommendations for enabling SME developers to play a more substantial role in housing delivery once again.

The key findings of the research include:

Timescales

- The average time from planning application submission to committee decision is 30 weeks.

- The average time from committee decision to formal permission being granted is 21 weeks.

- 44% of applications were determined by delegated powers, with an average timeline of 43 weeks.

- Applications determined at committee took 10 weeks longer on average – 53 weeks.

- 13% of sites took more than two years to achieve permission, and five sites under 30 units took over three years.

Costs

- Small sites faced average planning fees and obligations of approximately £2 million per site7.

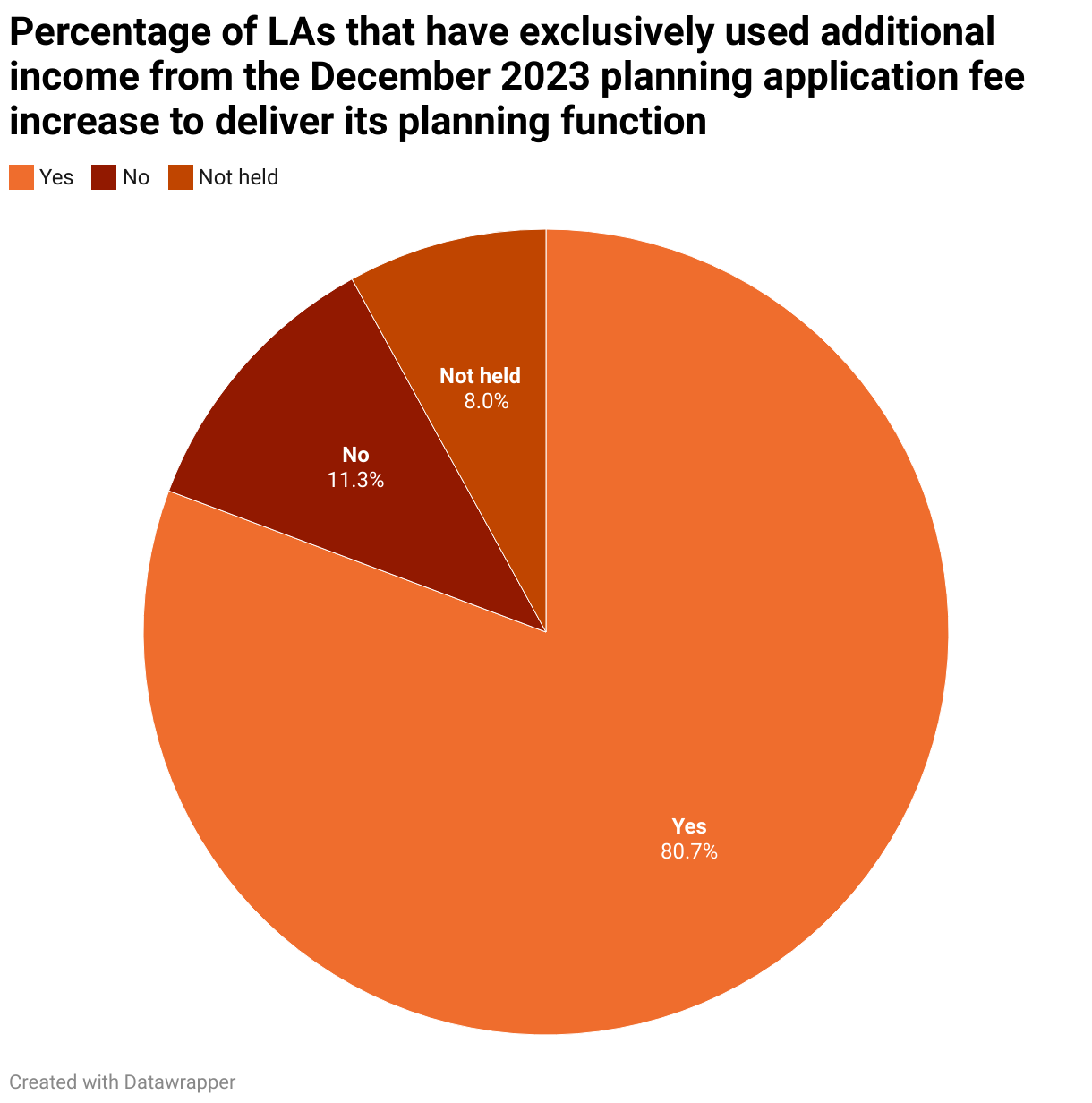

HBF also conducted a Freedom of Information (FOI) exercise to determine how Local Authorities had used the additional income generated from the planning application fee increased introduced on 6 December 2023. The research found…

Impact of increased planning fees

- 87% of Local Authorities have used the additional income generated from the planning application fee increase introduced on 6 December 2023 to exclusively support the delivery of their planning function.

- However, nearly a quarter (24%) of the 147 respondents indicated that the increased fees were still insufficient to cover the cost of running their planning departments.

Timescales

The analysis finds that the timescales facing planning applications for small sites vary significantly and are far longer than what could be considered reasonable or manageable. While delays are a known feature across all planning applications, they are especially burdensome for smaller builders – who are typically the primary developers of small sites. For these SME home builders, such delays can be financially and operationally detrimental, as they lack the capital reserves and pipeline flexibility of larger developers.

The CMA Market Study concluded that “Delays in the planning process have a disproportionate impact on SME housebuilders as they are required to hold on to a larger quantum of land for a longer period of time than they would otherwise and manage a longer period between paying the upfront cost associated with initiating a development and realising the returns from their investment.”

This challenge is underscored by the finding that it takes, on average, almost a year for planning permission to be granted on small urban sites. Specifically:

- The average time from planning application submission to committee decision is 30 weeks.

- The average time from committee decision to formal permission being granted is 21 weeks.

However, these averages conceal extreme variability. For example:

- One scheme for 89 homes in Leeds took 70 weeks just to reach committee decision.

- A 75-home site in Newcastle took 88 weeks from committee decision to final permission.

In terms of decision-making routes:

- 44% of applications were determined by delegated powers, with an average timeline of 43 weeks.

- Applications determined at committee took 10 weeks longer on average – 53 weeks.

Positively, in recognition of the delays caused by requiring planning applications to go before committee, the Government is now considering responses to the consultation to introduce a national scheme of delegation for planning decisions as part of a broader package of reforms to planning committees.

The changes would provide greater consistency and certainty about which decisions go to committee and will also:

- require separate, smaller committees for strategic development so there is more professional consideration of key developments; and

- introduce a requirement for mandatory training for all planning committee members so they are more informed about key planning principles.

When measured against statutory expectations, the current system is failing developers:

- Applications experienced an average 38-week delay beyond the statutory determination period.

- Only 6% of applications were determined within the statutory 13-week period, and just 14% met the 26-week Government planning guarantee.

- 13% of sites took more than two years to achieve permission, and five sites under 30 units took over three years.

Concerns raised

- There are a wide range of concerns flagged at committee for development at small sites across the wider cohort of sites.

- Architecture and design, and residential amenity impacts are amongst the top three concerns in six out of 10 cases.

- Viability and Affordable Housing is the top concern in 16% of cases, the third most significant after these.

These delays are compounded by further delays at every single stage of the planning process.

Additional research from HBF has found that:

- The average Section 106 agreement takes 515 days to complete.

- Home builders can be waiting up to 208 weeks for a Section 38 agreement to be approved.

These findings point to a systemic inefficiency in the planning process, with delays at every stage disproportionately affecting SME home builders. The compounded effect of prolonged determination periods, holdups by committee, and protracted legal agreements not only delays housing delivery but also discourages participation by smaller developers, ultimately hampering efforts to boost housing supply through a diverse and competitive market.

Costs

Outline permission costs

Over the past few decades, the cost of achieving a planning permission has steadily increased as the planning process has become more complex to navigate, and uncertainty has become a feature as builders secure an implementable planning consent.

The primary cause of these cost increases is the accumulation of additional policy requirements and the growing volume of supporting evidence required for each application8. Previous Lichfields research shows that permission on a small site now typically requires evidence from 10 to 12 consultants, with the cost of commissioning evidence from consultants for an outline permission on a small site increasing by 4.5 times in real terms since 1990, to an average of £125,0009.

The situation has been exacerbated by a loss of expertise and experience within LPAs, which has meant that councils have become more risk-averse and so demand additional evidence before giving outline permission10.

These initial, high upfront costs can deter SME home builders from growing their businesses and investing in new sites, as they will be reluctant to take on the risk of significant sunk costs within an already-uncertain planning system.

Cost of fees and planning obligations

The average small site faces planning fees and obligations of about £2 million11. This included:

- £18,600 in application fees

- £76,000 in professional fees

- £1.4 million Section 106 obligations

- £449,000 CIL payments (where applicable)

- £11,600 BNG delivery costs12

- An additional £170,000 in finance interest due to delays13.

Average costs will rise further with the planned introduction of the Building Safety Levy and Future Homes Standard within the next 18 months.

Planning costs are also relatively fixed regardless of site size, meaning that they are disproportionately high for smaller sites. CMA analysis shows that per-plot direct planning costs are:

- Around £3,500 on average for sites of fewer than 50 plots

- £1,500 for sites with 100-500 plots

- Under £1,000 for sites of more than 500 plots.

Given that SME home builders will naturally tend to seek smaller sites, this highlights the disproportionate financial burden placed on them by the planning system.

Furthermore, the estimated costs for a small site include an additional £170,000 in finance interest due to delays14. In recent years, new challenges have emerged, which have added to delays, such as the limited capacity of Registered Providers (RPs) to purchase Section 106 units and BNG implementation. Alongside a period of high interest rates, this has increased finance interest costs and placed additional strain on the cash flow of SMEs.

Planning fees

While application fees represent a relatively small expense compared to the other payments and obligations developers face when seeking planning permission, they are nonetheless an increasing concern for SME developers.

In December 2023, planning application fees were increased by 35% for sites of 10 or more homes, resulting in fees now being double their 1990 level in real terms and placing a further strain on SME developers.

Despite this, in recognition of the budgetary pressures Local Planning Authorities (LPAs) are facing, the home building industry was broadly, although not unanimously, supportive of the increases in planning fees.

However, this was conditional on the additional income being ringfenced for spending and investment in planning services and supported by a clear plan outlining how the services provided by local planning authorities (LPAs) will be improved as a result.

Consequently, the decision of the then Housing Secretary, Michael Gove, in 2023 not to legislate but to ringfence the fees came as a disappointment to home builders.

In its response to its consultation on the issue, the Government said: “We want to ensure that the fee increase results in additional funds being available to local authority planning departments, but we will not take ringfencing forward through legislation as this would impose a restriction on local authorities when they are best placed to make decisions about funding local services, including planning departments. However, we would expect local planning authorities to protect at least the income from the planning fee increase for direct investment in planning services”. It also stated that it “is expected that the performance of local planning authorities will improve”.

Following this decision, and with the sluggishness of the planning process continuing to be the top barrier facing SME home builders15, HBF was keen to understand how the increase in fees had been treated by LPAs and the potential impacts on the efficiency and speed of the planning process.

To that end, HBF submitted a Freedom of Information (FOI) request to local planning authorities to establish:

- Has the additional income generated from the planning application fee increase introduced on 6 December 2023 been used exclusively to support the delivery of the Local Authority’s planning function?

- What percentage of residential planning applications (minor and major), submitted after 6 December 2023, have resulted in an agreed Extension of Time?

In total, responses were received from 213 Local Authorities across England. Positively, in respect of Question One, it appears that most councils respected the Government’s direction that the income from the increased fees should be directly invested in development management services.

Despite concerns that unfenced fees might be diverted into councils’ general budgets, only 11.3% of responding councils reported this to be the case. Among them, one council noted a surplus that was subsequently shared with other departments.

However, while this may appear to be a positive outcome at first glance, it does not reflect the full picture. Many councils chose to provide further context in their responses, revealing that the fee increases have not delivered the benefits anticipated by the previous Government.

In practice, the assumption that the fee increase would generate additional income for local planning authorities appears to have been misplaced. Nearly a quarter (23.4%) of the 196 respondents that held data on their use of planning fees indicated that the increased fees were still insufficient to cover the cost of running their planning departments.

There were two common reasons given for the shortfall:

- The cost of running the planning function, even with the increase in fees, exceeds the amount of income received

“All fee income is allocated to supporting the general everyday functions of the planning service. Fee income does not typically cover the cost of providing the planning service.” - FOI respondent

“The additional income generated has been used to support the shortfall in funding to pay for the existing salary costs of Planning officers and Planning support officers”. – FOI respondent

“The additional income from the increase in planning fees have been used to help reduce the overall cost of the planning service. In 2024/25 when we budgeted for the extra increase, the Planning Service[‘s] net of income (including the additional income of £175k) was due to make a deficit of £2,227,200. That is just direct spend and income and doesn’t include any corporate overheads we would apportion to the planning service. The projected outturn for 2024/25 is a deficit of £1,549,948 which includes the additional income. This [is] for the whole planning service, so includes strategic planning, planning control and planning technical support”. – FOI respondent

- A decline in planning applications, leading to reduced fee income

“The additional income generated has been retained within the planning service. It is contributing towards helping fill an existing budget pressure that has arisen from reduced planning fee income over the last few years as we have seen a reduction in the number of planning applications submitted”. – FOI respondent

“Due to fewer applications being submitted, fee income has reduced”. – FOI respondent

Extension of Time agreements

Due to the ongoing funding and resourcing challenges among LPAs, it is unsurprising that Local Authorities are struggling to determine planning applications within the statutory timeframes.

In England, statutory timescales for LPAs are as follows:

- 13 weeks for applications for major development

- 10 weeks for applications for technical details consent, and applications for public service infrastructure development,

- 8 weeks for all other types of development (unless an application is subject to an Environmental Impact Assessment, in which case a 16-week limit applies).

However, if an application is likely to require additional time for determination, the Council and the applicant can enter into an Extension of Time (EoT) agreement. This allows the planning application to be considered beyond the statutory time limits of 8, 13, or 16 weeks16.

The Planning Advisory Service (PAS) states “for the overall credibility of the planning system, extensions of time should really be the exception and efforts made to meet the statutory timescale wherever possible” 17.

However, our research indicates that the use of Extensions of Time (EoTs) is far from uncommon. A total of 127 local authorities provided data on the percentage of residential planning applications (both minor and major) submitted after 6 December 2023 that resulted in an agreed Extension of Time. The findings were as follows:

- The average proportion of residential planning applications resulting in an agreed extension was 44.8%.

- The median proportion was 46.6%.

There is, of course, a legitimate need for EoTs. Delays can be caused by many factors, including:

- Slow responses from statutory consultees. HBF research has found that for Section 38 agreements, which relate to the construction of new highways, the time taken from technical submission to technical approval ranged from two weeks to 103 weeks, and to formal adoption ranged from four weeks to 286 weeks18.

- The length of time needed to agree Section 106 agreements. Our research found 35% of all S106 agreements took longer than 12 months to finalise19.

- Increasing policy and statutory requirements, e.g. Biodiversity Net Gain, being introduced at a time when funding and resources are already stretched.

However, it is evident that their use has become far more common than was originally intended and can mask the true performance and ability of Local Authorities in determining planning applications in a timely manner.

This was an issue that the former Housing Secretary, Michael Gove, attempted to address during the Government’s final year in power after data revealed “Approximately only 10% of local planning authorities determined 70% or more non-major applications within the statutory eight-week time limit, and 1% of local planning authorities determined 60% or more of major applications within the statutory 13- or 16-week time limits. This falls below government expectations for decision-making.” 20

Under Gove, the Government intended to change the use of extensions of time, including:

- Banning EoTs for householder applications

- Restricting when EoTs can be used during the decision-making process

- Prohibiting repeat EoT requests

- Publishing performance tables that exclude EoTs to expose poor performance

Due to the General Election taking place just two months after the conclusion of the consultation, the proposals failed to be implemented. However, a Public Accounts Committee session on developer funding (30 June 2025) suggested that the Labour Government is looking at this issue once again.

Joanna Key, Director General for Regeneration, Housing and Planning at the Ministry of Housing, Communities and Local Government (MHCLG) said during the session “what we are planning to do initially is to make it all much more transparent by publishing the information on the actual time. At the moment we say, “Have they decided the case within the period of time agreed?”, and that can include both the eight-week target and the extension. The intention now is to produce that information so that it is very clear which authorities have delivered within the statutory timetables”.21

Encouragingly, William Burgon, Director for Planning at MHCLG also said: “Ministers are also looking to make greater use of the performance system that they have available, whereby they can designate an authority for lack of timeliness and, linked to that, poor performance. You have seen a number of authorities be designated on those grounds in the last year, and you would expect to see Ministers continue to be quite robust on that front, because they have been clear that on not only plan making - where, as we have discussed, we have been making more interventions - but decision making they are keen to use the powers available to them to drive home the fact that, exactly as you say, the statutory timelines are there for a reason.” 22

An increased level of transparency regarding timelines is a positive step. However, it is important to remember that the increasing use of EoT by LPAs is simply another symptom of chronically-underfunded and under-resourced LPAs.

Further increases

The Government, to its credit, is taking action to put LPAs on a self-sustaining footing. Through the Planning and Infrastructure Bill, local authorities will be given more autonomy to set their own fees to achieve cost recovery for applications.

Specifically, it is pursuing a fees model that allows for local variation from a national default fee. The Government anticipates that this approach will give LPAs greater flexibility to fund and deliver an effective service whilst preventing large differences in fees between LPAs.

This, as our research has demonstrated, is crucial as the current fees do not allow for the delivery of planning services to be fully funded. Nevertheless, at a challenging time for the industry it is worrying that fees are set to increase further, particularly as the uptick in fees may have a disproportionate effect on SMEs.

Indeed, the Bill’s impact assessment warns that fee increases will significantly affect SMEs because minor applications are estimated to have the greatest funding gaps of between 50% and 150%. As the assessment says, “if LPAs set fees at the level of full cost recovery, it is likely that the fees for minor applications will proportionately increase by a greater rate than fees for major applications.”

Given the sheer scale of the deficit that some LPAs are facing in their funding, the increase in fees has the potential to be significant.

“The total expenditure for the DM function in 2024/25 was £4,251k (including £1,436k Corporate Overheads). The total income, inclusive of the additional income, was £2,801k. This gives a net cost of £1,450k. This is a net cost to the Local Authority's general fund” – FOI respondent.

Conclusions and recommendations

Recently the Government has announced a range of measures which it considers will help support SME developers. These include:

- ensuring all applications for Reserved Matters approvals and developments of nine homes or fewer are delegated to planning officers;

- introducing a new ‘medium site’ category of 10 to 49 homes;

- streamlining of BNG requirements, including extending use of the Small Sites Metric to medium sites;

- reviewing requirements for smaller sites to require consultation with statutory consultees;

- and exploring exempting developments of 49 or fewer homes from the Building Safety Levy23.

While these developments have been broadly welcomed by the industry, SME home builders continue to face a range of persistent challenges and constraints that hinder their ability to bring forward new sites.

To further support this vital part of the industry, and increase housing delivery, the Government should go further to speed up the planning process.

1. Ensure LPAs are sufficiently staffed and resourced

As highlighted throughout this report, LPAs are currently facing significant resource constraints, which affect their capacity to process planning applications promptly. Recent FOI research carried out by HBF shows that 80% of councils are operating at below full staffing capacity in their planning departments. While the Government has so far announced plans to support local authorities with 300 additional junior planning officers across the country, HBF estimates that there is a national shortage of 2,200 planners.

Planning delays caused by insufficient LPA resourcing disproportionately affect SMEs. To alleviate these challenges, the Government should allocate targeted funding to increase staffing levels within planning departments. This should include increasing the number of additional planning officers it is currently aiming to recruit to local authorities through an increase in government funding to the Planning Delivery Skills Fund, so that it more accurately reflects the current skills gap.

2. Introduce common adoptable standards for infrastructure and mandatory adoption within sensible timeframes

Where infrastructure has been fully constructed, is operational and is being utilised by the public for the purpose to which it was intended, then there should exist an obligation for a mandatory adoption.

A national standard is also needed to implement statutory timescales for Section 278 and Section 38 highways agreements. After such time has elapsed, outstanding applications would be deemed approved. This will reduce the cost and bureaucratic burden for all sites, but would particularly benefit SMEs.

3. Introduce a standard template for Section 106 agreements

A lack of standardisation in the drafting of Section 106 agreements often leads to protracted negotiations and inconsistencies across councils, with 76% of local authorities reporting average negotiation timescales exceeding 12 months. The Government, in collaboration with planning authorities and the development sector, should produce standardised procedural guidelines and clauses to minimise the need to draft agreements from scratch. In lieu of official standardisation, there could be clearer guidance and expectations on good practice.

4. Encourage a more flexible use of cascade agreements on Section 106 Affordable Housing units where necessary

With the declining interest of Registered Providers (RPs) in purchasing Section 106 Affordable Homes, many SMEs are experiencing delays due to the length of time taken to find a purchaser (if one can be found at all) or engaging in protracted negotiations with LPAs to secure a Deed of Variation to existing Section 106 agreements.

To tackle this issue, the Government should issue a Written Ministerial Statement encouraging LPAs to take a more flexible approach to the use of cascade mechanisms in Section 106 agreements and the renegotiation of existing agreements. This would give reassurance to the developer that if an RP cannot be found, the Affordable Homes can be changed to an alternative tenure or, as a last resort, a payment in lieu of Affordable Housing.

5. Fast track the scheme of delegation and ensure it benefits SMEs

The Government should provide clarity as soon as possible on the design of its scheme of delegation, so that it is ready to be introduced as soon as the Planning and Infrastructure Bill becomes law.

It should proceed with its proposal that small sites are always delegated to planning officers, with medium sites also exempted in some circumstances.

6. Use National Development Management Policies (NDMPs) to support the quick delivery of small brownfield sites

The Government could issue an NDMP stating that planning applications for homes on brownfield and Grey Belt land of less than one hectare (the proposed threshold for major development) are to be approved.

NDMPs override other conflicting development plan policies, so they would provide a simple and direct means by which more land for SMEs can be released quickly.

7. Make sure small local habitat banks are available at a reasonable cost for SME home builders to support the delivery of BNG

In many cases, off-site biodiversity units at an appropriate size and cost are unavailable for SMEs. This is because small sites often require only fractions of a biodiversity unit to meet BNG requirements, but the market has not yet developed sufficiently to meet this demand.

While the proposals to simplify BNG are very welcome, there will still be significant reliance on the off-site market on medium sites. The Government should renew its efforts to increase private investment in the market and the availability of small local habitat banks.

On the forthcoming changes to planning fees, we encourage the Government to:

1. Provide certainty on the national default fee level.

The Government must provide early and clear guidance on how this default fee will be calculated, the frequency of its review, and the principles that will underpin it so that developers and LPAs have transparency

2. Define what constitutes a cost recovery basis.

The concept of "full cost recovery" must be clearly articulated. This should include guidance on which costs can be legitimately recovered through fees such as staff costs, training, IT systems, enforcement functions, and overheads. Without a standardised definition, there is a risk of inconsistency across authorities.

3. Clarify how it will support LPAs facing a drop in applications.

It is also essential to understand how the Government intends to support those LPAs that are seeing significant drops in application volumes, as even full cost recovery may not be achievable in areas with limited development activity.

4. Closely monitor the performance of LPAs.

The Government must closely monitor the performance of Local Planning Authorities (LPAs) to ensure that any additional costs are matched by tangible and measurable improvements. In particular, developers should see considerable gains in the speed and efficiency with which both LPAs and statutory consultees determine planning applications and discharge conditions.

Footnotes

- This aligns with the definition used by Lichfields in their 2020 report on small sites in London, which this report expands on.

- The Housing Pipeline Report does track permissions for sites of 1 & 2 units, but these have an average site size of around 1.1 unit sites. These numbers have therefore been excluded from this analysis as they are primarily single unit sites, such as self-build sites, and therefore distort the totals.

- We have excluded from this analysis sites of 1-2 homes. Because of the categorisation, these overwhelmingly pick up sites of a single new home which may not generally be constructed by home builders and cannot be considered ‘home building sites’ if it is for a single dwelling.

- HBF Slow Lane to Adoption 2025

- MHCLG, Planning and Infrastructure Bill: Impact assessment, 6 May 2025

- Lichfields/Pocket Living, Small Sites: Unlocking housing delivery, September 2020

- Based on an average across the sample (Median: 16 homes)

- As noted by the Competition and Markets Authority (CMA) in its housebuilding market study.

- Lichfields, Small builders, big burdens, 2023. Based on estimates for an illustrative green field site of around 40 homes.

- Ibid.

- Based on an average across the sample (Median: 16 homes)

- Small sites of 10 units or under may soon be exempted from BNG. Estimate based on Defra impact assessment modelling.

- Assuming an average 38-week delay in securing a permission and an average 12% finance agreement, excluding extension fees.

- Based on finance interest payments accrued for planning fees and developer contributions during the delay only.

- HBF/Close Brothers Property Finance/Travis Perkins, State of Play, 2024-25

- JWPC Chartered Town Planner, Have Extensions of Time for planning applications worked?, December 2024

- PAS, Decisions - Positive planning Questions and answers on Agreements to extend the time for decision

- HBF Slow Lane to Adoption 2025

- HBF, What is the timeframe for local authorities to agree community investment? 2025

- DLUHC, An accelerated planning system, 6 March 2024

- House of Commons Public Accounts Committee, Oral evidence: Improving local areas through developer funding, 30 June 2025

- Ibid.

- MHCLG, Government backs SME builders to get Britain building, 28 May 2025.